Evolution of Money, Banking and Financial Crisis

History, Theory and Policy

Summary

focuses primarily on the historical development of money, the change of the banking sector and global financial crises. Money, which started as an exchange tool and has become digital; historical change in the banking system and its relationship with policymakers; global financial crises, balloons, and speculations and policies for the emergence and prevention of them are thoroughly examined in the book.

Excerpt

Table Of Contents

- Cover

- Title

- Copyright

- About the editors

- About the book

- This eBook can be cited

- Preface and Acknowledgments

- Contents

- List of Contributors

- Section 1 Money, Exchange Rate, and Finance

- 1 Exchange Rate Regimes and the Financial Trilemma: An Evaluation for the Post-Bretton Woods (Ünay Tamgaç Tezcan)

- 2 Searching for the Roots of Cryptocurrency Throughout History: An Analysis of Bitcoin (Cem Berk)

- 3 Exchange Rate Pass-Through to Inflation: The Case of Turkey (Pınar Koç)

- 4 Nonlinear Exchange Rate Pass-Through to Inflation: A Comparison of Turkey and BRICS Countries (Aydanur Gacener Atış, Deniz Erer and Elif Erer)

- 5 The Relationship Between Finance and Growth in North African Countries: Fresh Evidence from Panel Causality (Erdal Tanas Karagöl, Önder Özgür and Muhammed Şehid Görüş)

- Section 2 Financial Systems, Stock Markets, and Financial Crisis

- 6 Exchange Rate Uncertainty and Dollarization in Turkey (Yavuz Selim Hacıhasanoğlu and Mehmet Selman Çolak)

- 7 Banking, Currency and Fiscal Crisis (Berna Serener)

- 8 Financial Systems Importance, Differences, and Convergence (Tuba Gülcemal)

- 9 Financial Speculation and Bubble: An Empirical Investigation of Bubble in the Turkish Stock Market (Eyyüp Ensari Şahin)

- 10 Islamic Finance in the Framework of Financial Crisis and the Evaluation of Islamic Finance (Mustafa Kevser and Mesut Doğan)

- 11 Analysis of Reserve Option Mechanism Applied for Providing Financial Stability (S. Nurbanu Yıldız and Üzeyir Aydın)

- 12 An Econometric Analysis of the Current Account Deficit-External Debt Relationship: The Case of Turkey (Mehmet Barış Aslan)

- 13 Impact of Financial Development on Current Deficit in Turkey: ARDL Bound Test Analysis (Zeki Akbakay)

- 14 Effect of Financing Resources on Profit, Investment, and Firm Value: Comparison of BIST and NYSE (Hakan Altin and Cemil Süslü)

- 15 Investigation of Weak Form Market Efficiency of EU Country Stock Markets in the Crisis Period (İhsan Erdem Kayral)

- 16 Towards an Activist Monetary Policy: Challenges for Central Banking in the Post-Crisis Era (Metin Özdemir and Ali İlhan)

- Section 3 Banking and Risk Management

- 17 Assessing Credit Cycle Dynamics in the Turkish Banking Sector (İ. Ethem Güney, M. Selman Çolak and M. Hasan Yılmaz)

- 18 The Effect of Basel Regulations on Banking Efficiency: Evidence from Turkey (Ramazan Ekinci)

- 19 Long-Term Analysis of Riskiness in the Turkish Banking Sector (Sema Bayraktar and Sercan Koyunlu)

- 20 The Determinants of Bank’s Stock Volatility (Emre Esat Topaloğlu, Reşat Sakur and Serdar Yaman)

- 21 Determinants of Non-performing Loans: Evidence from the Turkish Banking Sector (Pınar Karahan-Dursun)

- List of Figures and Graphs

- List of Tables

List of Contributors

Ali İlhan

Dr., Tekirdağ Namık Kemal University

ailhan@nku.edu.tr

Aydanur Gacener Atış

Assoc. Prof., Ege University

aydanur.gacener@ege.edu.tr

Berna Serener

Asst. Prof., European University of Lefke

bserener@eul.edu.tr

Cem Berk

Assoc. Prof., Kırklareli University

cem.berk@klu.edu.tr

Cemil Süslü

Dr. Iskenderun Technical University

cemil.suslu@iste.edu.tr

Deniz Erer

PhD in Economics, Independent Researcher

denizerer@hotmail.com

Elif Erer

PhD in Economics, Independent Researcher

elif_erer@hotmail.com

Emre Esat Topaloğlu

Asst. Prof., Şırnak Üniversity

emresatopal@qhotmail.com

Erdal Tanas Karagöl

Prof. Dr., Ankara Yıldırım Beyazıt University,

Ankara, Turkey

erdalkaragol@hotmail.com

Eyüp Ensari Şahin

Asst. Prof., Hitit University

eyupensarisahin@hitit.edu.tr.

Hakan Altın

Assoc. Prof., Aksaray University

hakanaltin@aksaray.edu.tr

İbrahim Ethem Güney

Dr., Central Bank of the Republic of Turkey

ethem.guney@tcmb.gov.tr

İhsan Erdem Kayral

Asst. Prof., Konya Food and Agriculture University

erdem.kayral@gidatarim.edu.tr

Mehmet Barış Aslan

Asst. Prof., Bingöl University

mbaslan@bingol.edu.tr

Mehmet Selman Çolak

Asst. Economist, Central Bank of the Republic of Turkey

selman.colak@tcmb.gov.tr

Mesut Doğan

Assoc. Prof., Afyonkocatepe University

mesutdogan07@gmail.com

Metin Özdemir

Assoc. Prof., Bursa Uludağ University

mozdemir@uludag.edu.tr.

Muhammed Hasan Yılmaz

Asst. Economist, Central Bank of the Republic of Turkey

muhammed.yilmaz@tcmb.gov.tr

Muhammed Şehid Görüş

Research Assistant, Yıldırım Beyazıt University

msgorus@ybu.edu.tr

Mustafa Kevser

Asst. Prof., Bandirma Onyedi Eylul University

mkevser@bandirma.edu.tr

Nurbanu Yıldız

Master’s Degree, Independent Researcher

nurbanu.koyukan@gmail.com

Önder Özgür

Research Assistant, Yıldırım Beyazıt University

oozgur@ybu.edu.tr

Pınar Karahan-Dursun

Dr., Anadolu University

pkarahan@anadolu.edu.tr

Pınar Koç Torun

Asst. Prof., Gümüşhane University

pinartorun@gumushane.edu.tr

Ramazan Ekinci

Asst. Prof., İzmir Bakırçay Üniversity

ramazan.ekinci@bakircay.edu.tr

Reşat Sakur

Asst. Prof., Şırnak Üniversity

resatsakur@hotmail.com

Sema Bayraktar

Asst. Prof., İstanbul Bilgi University

sema.bayraktar@bilgi.edu.tr

Sercan Koyunlu

Master’s Degree, Independent Researcher

İstanbul Bilgi University

sercankoyunlu@hotmail.com

Serdar Yaman

Lec., Şırnak Üniversity

srdr73@gmail.com

Tuba Gülcemal

Asst. Prof., Cumhuriyet University

tgulcemal@cumhuriyet.edu.tr

Ünay Tamgaç Tezcan

Asst. Prof., TOBB University

utamgac@etu.edu.tr; unaytamgac@gmail.com.

Üzeyir Aydın

Assoc. Prof., Dokuz Eylul University

uzeyir.aydin@deu.edu.tr

Yavuz Selim Hacıhasanoğlu

Central Bank of the Republic of Turkey

Yavuz.Selim@tcmb.gov.tr

Zeki Akbakay

Asst. Prof., Bingol University

zekiakbakay@gmail.com

Ünay Tamgaç Tezcan

1 Exchange Rate Regimes and the

Financial Trilemma: An Evaluation for the

Post-Bretton Woods

Highlights: The choice of the exchange rate regime is one of the most argued topics in economic policy. Since the collapse of the Bretton Woods system, countries have adopted different exchange rate arrangements. In this chapter we make an evaluation of the discussions around the regime choice, and the financial trilemma. Our main focus is to provide a historic review on this discussion and how it has translated itself after the global financial crisis. More recently, the trilemma view has been brought into question after the global financial crisis. Rey (2015, 2016) argues that “whenever capital is freely mobile, the global financial cycle constrains national monetary policies regardless of the exchange rate regime.” Accordingly, the classical monetary trilemma transforms into a “dilemma” or an “irreconcilable duo” where the exchange rate regime loses importance. We discuss whether the trilemma prevails and exchange rates provide effective insulating mechanisms. While the debate is still ongoing the strong standing argument is that exchange rate regime still matters. The trade-off between exchange rate stability, monetary policy autonomy, and financial integration also hold. However, with the size of global linkages the trade-offs have become harsher.

Keywords: Exchange rate regime, monetary policy autonomy, financials integration, open economy trilemma, dilemma hypothesis

Introduction

The unprecedented financial turmoil that started with the collapse of the giant Lehman Brothers in September 2008 can be regarded as a turning point in economics thinking. As the capitalist system was brought under question, the basic assumptions of fundamental economic theory, and policy making also took its toll. New questions on how the real economy and financial markets work and their interconnectedness brought in new considerations into light. The global financial crisis (GFC) has made evident the existence of global cycles.

After the crisis, a large literature evolved that analyzes the determinants of global cycles, synchronization in countries, and asset price co-movements (For a survey see Claessens and Kose 2017). One important takeout is that global financial linkages and especially global spillovers from the USA have become ←13 | 14→a dominating power in the global economy. There is a vast literature that investigates the cause and effects of these spillovers. The main driver is the capital mobility and financial connectedness. Rey (2015) points out that the “global financial cycle” created by the monetary policy in the center country, that is, the USA, affects the capital flows and credit growth in the international financial system through leverage of global banks (Cerutti, Stijn & Ratnovski, 2017).

One related question is how countries can insulate themselves from the negative effects of the global spillovers. This has brought into question how countries under different arrangements are affected by global spillovers and whether exchange rates provide effective insulating mechanisms. In light of the recent evidence, we revisit this important concept in international finance, which is the exchange rate regime choice. Our main focus is to provide a historic review on this discussion and how the question has translated after the GFC.

The choice of the exchange rate regime is one of the most discussed subjects in economic policy making. Since the collapse of the Bretton Woods system, countries have adopted different exchange rate arrangements. While there is an extensive literature on comparison of the exchange rate regimes with respect to different performance measures, the literature fails to provide a clear cut answer. The GFC has once again shown that in the countries’ quest for economic stability and growth, the exchange rate system deems to stay as an important policy issue. One argument is that with today’s strong global interlinkages, monetary policies are constrained regardless of the exchange rate regime. This view has started a discussion on whether the exchange rate regime matters for monetary policy autonomy, and put the regime change into question. In this chapter, we intend to analyze the exchange rate regime choice in relation to this ongoing debate. In doing so, we will first look at how the system evolved after collapse of the Bretton Woods system, and we will discuss the changing pattern of exchange rate arrangements in the post-Bretton Woods world. One point we will pay attention to is the evolution of the financial architecture, specifically the changing pattern of “financial trilemma” among countries, and whether the traditional trilemma prevails under this new system of increased financial linkages.

The rest of the chapter is organized as follows. In this chapter, we start with a brief historic discussion on the evolution of the exchange rate system. Drawing on the experience of the countries with various exchange rate regimes since the 1980s, we summarize some of the findings around exchange rate regimes: the bipolar hypothesis in Section 3 and the exchange rate regime choice in Section 4. Then we discuss the trilemma view, and the debate that started after the GFC. Finally, the discussion is summarized, and some policy implications are presented.

←14 | 15→1 Historic Overview

After the collapse of the Bretton Woods system, from 1973 till 1994, the world entered a period of increased globalization and financial liberalization. This period is known as the “modern era of financial globalization”. There has been a steady increase in financial integration with the capital account liberalizations in advanced economies in the 1980s and in emerging markets in the 1990s.

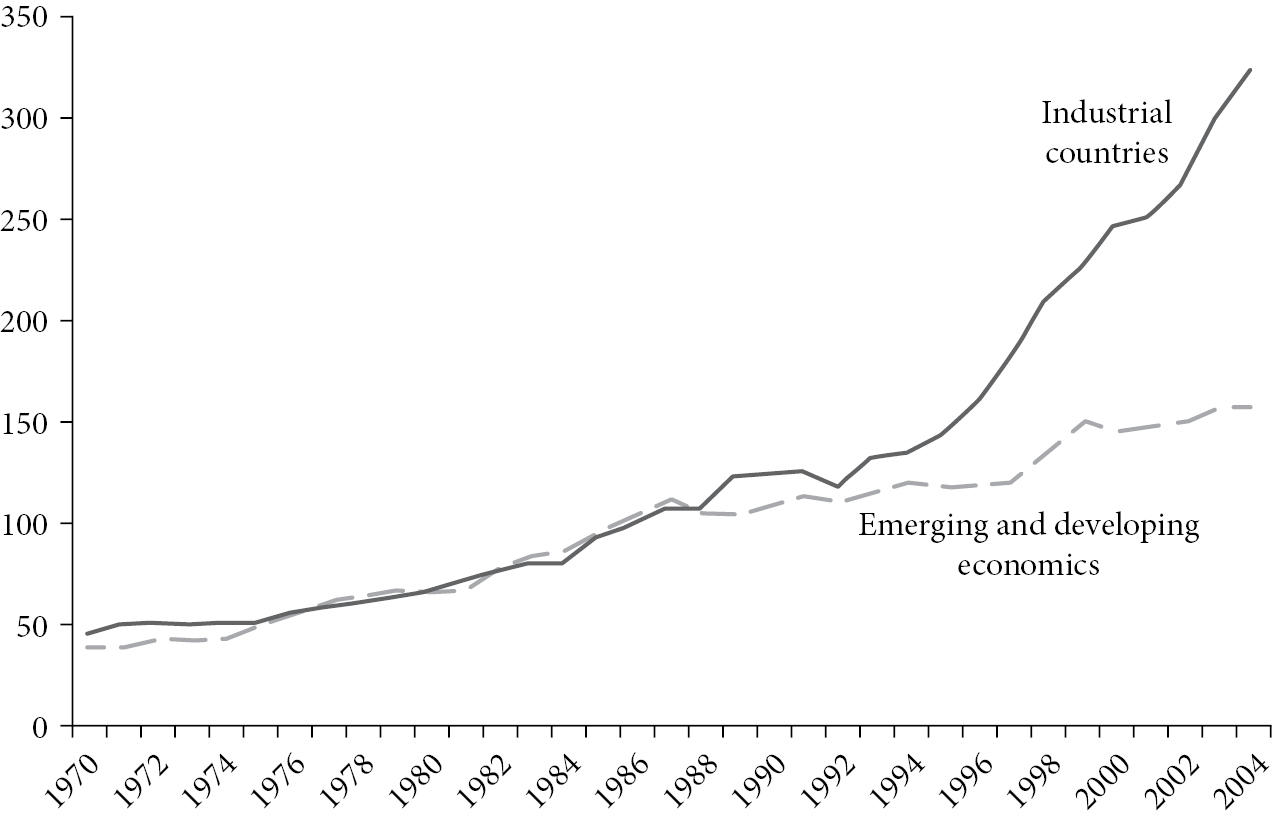

The sum of foreign assets and liabilities over GDP, plotted in Fig. 1.1, which is a measure of international financial integration, has increased by a factor of 7, from 45 % in 1970 to over 300 % in 2004 (Lane & Milesi-Ferretti, 2007). During the 1970s and 1980s, the increase was fairly gradual, but since the mid-1990s there has been an acceleration for the emerging markets/developing countries.

Fig. 1.1: International financial integration, 1970–2004

Notes: Ratio of sum of foreign assets and liabilities to GDP, 1970–2004. Source: Lane & Milesi-Ferretti, 2007

Whether international financial integration was, in fact, stronger in the first era of financial globalization (pre 1913 period) has been an issue of debate among economists. While some stated that the early period was more globalized (e.g., Bordo & Flandreau, 2003; Bordo & Murshid, 2006; and Quinn, 2003), some claim otherwise (Mauro et al., 2002; and Quinn & Voth, 2008). Some studies characterize the world financial integration by a U-shape with almost equal ←15 | 16→integration before 1914 and after 1970 (Bordo & Flandreau, 2003; Obstfeld & Taylor, 2003, 2004; and Goetzmann et al., 2005). Volosovych (2011) finds support for a J-shape pattern with a trough in the 1920s.

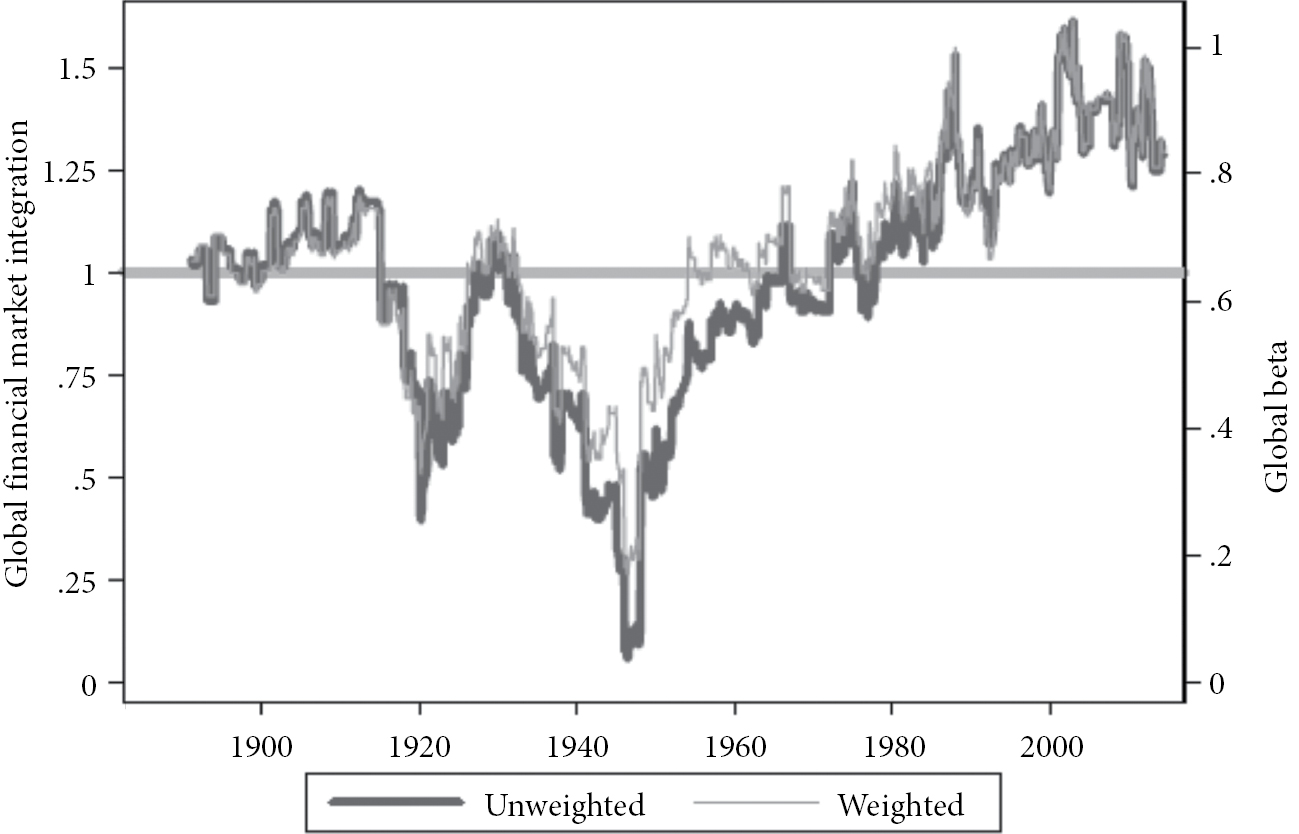

In a recent study, Bekaert and Mehl (2019) using a sample of 17 economies accounting for two-thirds of world GDP over the sample period from 1885 to 2014 show that the pattern follows a “swoosh” shape (see Fig. 1.2).1 There is high financial market integration in the pre-1913 period, still higher in the post-1990, and low in the interwar period. Their finding is in line with Rangvid et al. (2016) who look at equity market integration for the period 1875–2012 and find much higher financial integration in the later part of their sample relative to earlier.

Fig. 1.2: Global financial integration, 1885–2014

Notes: Thick gray lines show the unweighted and light gray lines show the value-weighted cross-country averages of the global financial market integration measures and the corresponding conditional beta estimates. Source: Bekaert & Mehl (2019: 234)

Most emerging economies had maintained open capital accounts by the end of 1990s. The liberalization period in the emerging economies (the middle- and low-income economies) was one with frequent crises and output losses. In their struggle to fight inflation, these countries adopted fixed exchange rate regimes as a tool to import credibility in the monetary policy (Edwards, 2001). However, most of these attempted ended with a demise.2 Starting with the tequila crisis 1994 in Mexico, many emerging economies experienced balance of payments crises accompanied by painful devaluations and output losses.3 As both empirical and theoretical studies attempted to investigate the underlying causes and consequences of these episodes, a vast literature emerged on different types of currency crises models. (see Krugman, 1979; Flood & Garber, 1984; Obstfeld, 1986; Jeanne, 1997 for crisis literature and Kaminsky, Lizondo, Reinhart, 1998; Kaminsky, 2006 among others for crisis determinants).

2 Bipolar View

After the experience with the fragility of fixed exchange rate regimes in the 1990s, more emerging countries chose to adopt floating regimes that insulated them from the risks of speculative attacks (e.g., Indonesia, South Korea, and South Africa). The move towards exchange rate flexibility is most evident in developing Asia and Latin America. Emerging Asian economies shared this trend until 2000, at which time exchange rate stability started increasing. Some others kept operating under more rigid arrangements (e.g., Argentina and Malaysia).

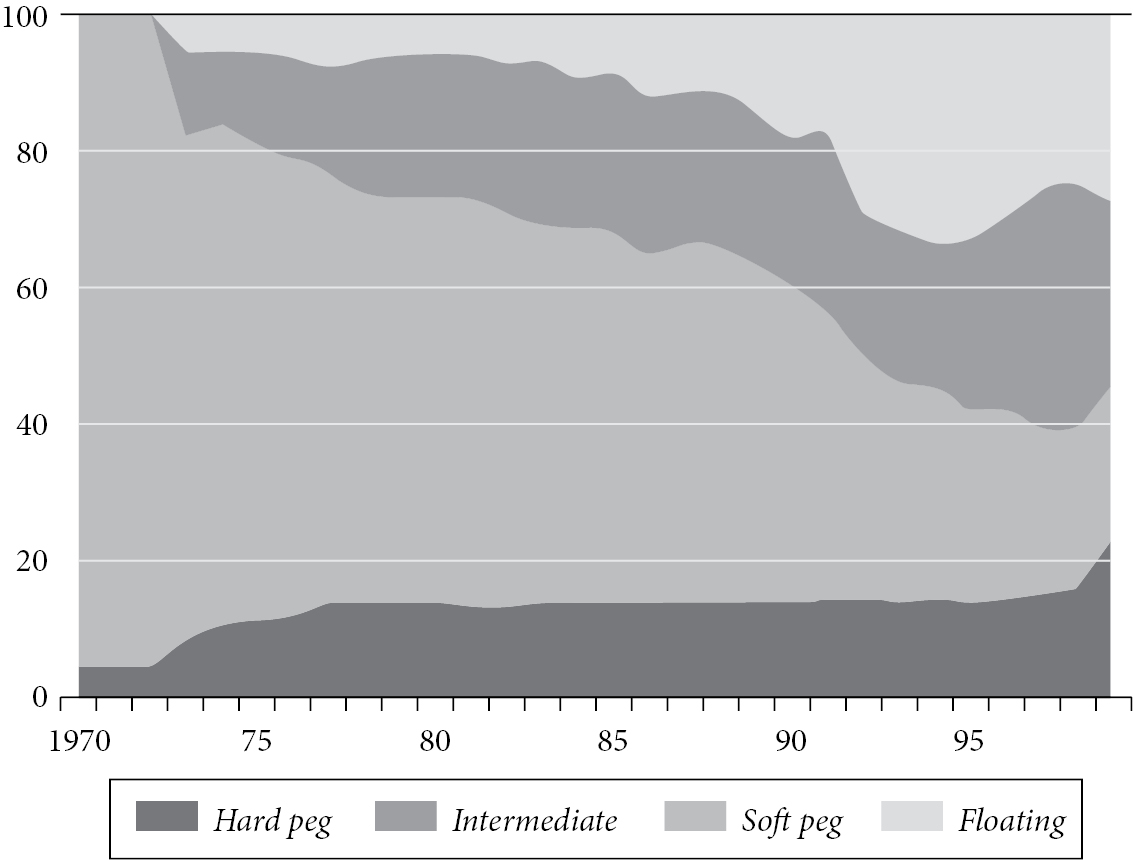

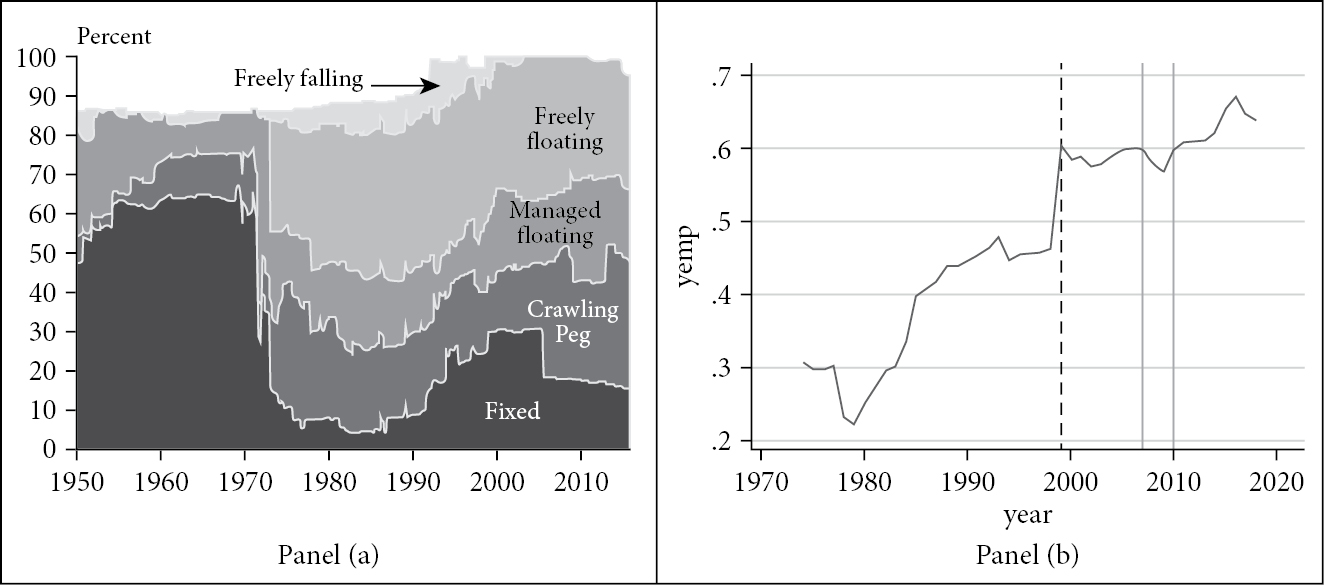

In the 2000s pointing out to this divergence, several studies claimed that there has been a move towards the corner regimes of floating or pegged arrangements, known as the “bipolar view” (Eichengreen, 1994; Fischer, 2001; Summers, 2000). The declining share of the intermediate regimes in the de-jure classification supported the bipolar view (see Fig. 1.3).

Fig. 1.3: Evolution of exchange rate regimes, 1970–2000

Source: Ghosh, Gulde, Wolf (2003) and IMF staff estimates

The argument was that for countries well integrated into world capital markets, intermediate regimes (or soft pegs) are crisis-prone and unsustainable, also known as the “the vanishing-middle” (Eichengreen, 1994) or “hollowing-out” ←17 | 18→hypothesis (Fischer, 2001). Obstfeld and Rogoff (1995, p. 74) claim that for countries with an open capital “there is little, if any, feasible middle ground between floating rates and the adoption of a common currency.”

Ghosh, Gulde, and Wolf (2003); Levy-Yeyati and Sturzenegger (2005); Bubula and Otker-Robe (2002); and Fischer (2001) are other examples that pointed out to the declining share of countries with intermediate exchange rate arrangements. However not all studies found support for the bipolar argument (e.g., Bubula & Otker-Robe, 2002). Some studies showed that the shares of the three main regimes was essentially unchanged (Rogoff et al., 2004; Dubas, Lee & Mark, 2005) or rose (Bailliu, Lafrance & Perrault, 2003) since the early 1980s.4

One reason for the mixed finding is related with how the exchange rate regimes were defined and specifically how the regimes are aggregated into categories. For example, Bubula and Otker-Robe (2002) and Fischer (2001) (both ←18 | 19→who used the IMF de facto coding) classified the “managed floating” into the floating corner. Also because of the fear of floating, many countries that claimed to operate under floating regimes actually did not.

Nearly a decade after the famous bipolar argument, we see a continued presence of intermediate regimes such as soft pegs confirming Bubula and Ötker-Robe’s (2002) argument that intermediate regimes are unlikely to disappear in the future. Also some countries flip back and forth between pegs and floats (Klein & Shambaugh, 2008).

In Figure 1.4 panel (a) shows the share of world GDP in each category of the de facto classification constructed by Ilzetzki, Reinhart, and Rogoff (2019). As can be seen, while there has been an upward trend in fixed arrangements after the 1980s, there is no validation of the bipolar hypothesis. In a recent study, Frankel (2019) constructed a continuous measure of de facto exchange rate regime classification for 145 countries in the post-Bretton Woods period from July 1974 to May 2018. The measure ranges between 0 and 1 corresponding to the hard peg and pure floating corners, and in Fig. 1.3 panel (b) shows the arithmetic mean value of the continuous ERR measure for all countries. As can be seen, there is an increasing trend towards flexible regimes, also invalidating the bipolar view. Since 2000, developing countries have converged towards managed exchange rate flexibility. Majority of the advanced economies are operating ←19 | 20→either under a floating regime or are members of the euro zone. Emerging economies have a greater diversity in exchange rate regimes, and the exchange rate regime choice is still a live policy issue.

Fig. 1.4: Recent evolution of exchange rate regimes

Notes: Panel (a) shows the de facto exchange rate arrangements, coarse classification, 1946–2016: Share of world GDP in each group. Source: Ilzetzki, Reinhart and Rogoff (2019). Panel (b) shows the arithmetic mean value of the continuous de facto exchange rate regime flexibility index for 145 countries. Source: Frankel (2019)

3 Exchange Rate Regime Choice

There is a large literature on the optimal exchange rate regime choice which has extended after the collapse of the Bretton Woods system. These studies provide theoretical arguments for floating versus pegging the exchange rate. This literature examines the macroeconomic conditions that affect the regime choice and under what circumstances which exchange rate regime delivers the optimal results (e.g. Rizzo, 1998; Edwards, 1999). (For a summary on the empirical findings on the exchange rate regime choice see Rogoff et al., 20034 and von Hagen and Zhou, 2007).

One of the main supporting arguments for fixed exchange rates is the predictability they provide. Related to that is their trade enhancing function through reduced uncertainty as predicted by the optimum currency area (OCA) theories (McKinnon, 1963). On the negative side, fixed regimes fail to provide the automatic adjustment mechanism to bring the economy back to full employment when hit by a negative shock. Also they can lead to prolonged overvaluations that can hamper the economy, and are susceptible to speculative attacks.

Considering that prices are highly inflexible in the short run, flexible exchange rate regimes provide the advantage by allowing automatic adjustment of the real exchange rate when the economy is hit by an aggregate demand or supply shock (Bailliu, Lafrance, & Perrault, 2003). Also they allow the monetary policy to respond to such shocks and dampen the negative effect on the economy.

Besides the price stability advantage of fixed exchange rates, another argument is that they can act as a disciplining device in fight for inflation (Giavazzi & Giovannini, 1990). A credible fixed exchange rate replaces bad domestic monetary policy with good foreign monetary policy (see Calvo & Reinhart, 2000). However imperfect credibility of fixed exchange rates has made them subject to runs and crises, making them costly policy alternatives (see Carmignani, Colombo & Tirelli, 2005).

Details

- Pages

- 364

- Publication Year

- 2020

- ISBN (Softcover)

- 9783631817933

- ISBN (PDF)

- 9783631835456

- ISBN (ePUB)

- 9783631835463

- ISBN (MOBI)

- 9783631835470

- DOI

- 10.3726/b17593

- Language

- English

- Publication date

- 2020 (September)

- Keywords

- Money Banking Financial markets Financial crisis Exchange rate regime Blockchain Digital currency Financial economics Stock markets

- Published

- Berlin, Bern, Bruxelles, New York, Oxford, Warszawa, Wien, 2020. 364 pp., 40 fig. b/w, 64 tables.

- Product Safety

- Peter Lang Group AG

Biographical notes

Çağatay Başarir (Volume editor) ![]() Burak Darici (Volume editor)

Burak Darici (Volume editor)

Burak Darici is a professor at Bandırma Onyedi Eylül University, Turkey. His main interests are monetary policy, labour market, financial markets and international economics. Çağatay Başarir is an associate professor at Bandirma Onyedi Eylul University, Turkey. His main interests are financial markets, portfolio management and international finance.