Performance Measurement Systems

Design and Adoption in German Multinational Companies

Summary

Excerpt

Table Of Contents

- Cover

- Title Page

- Copyright

- About the author

- About the book

- Preface

- Acknowledgements

- Contents

- 1 Introduction

- 1.1 Motivation and research questions

- 1.2 Scientific positioning

- 1.3 Outline of the study

- 2 Conceptual basis

- 2.1 Definition of multinational companies

- 2.2 Objectives of parent-PMSs

- 2.3 Design of parent-PMSs

- 2.4 Adoption of parent-PMSs

- 3 Review of prior research

- 3.1 Overview of the literature

- 3.2 Design of parent-PMSs

- 3.3 Adoption of parent-PMSs

- 3.4 Summary and research gaps

- 4 Theory

- 4.1 Introduction to New Institutional Sociology

- 4.2 Isomorphism and institutional pressures

- 4.3 Responses to institutional pressures

- 4.4 Influencing factors of responses to institutional pressures

- 4.5 Summary of the theoretical framework

- 5 Empirical research approach

- 5.1 Selection rationale

- 5.2 Research design

- 5.3 Research process

- 6 Empirical results

- 6.1 Within-case analyses

- 6.2 Cross-case analyses

- 7 Conclusions

- 7.1 Main results and implications

- 7.2 Limitations and future research

1Introduction

1.1Motivation and research questions

Multinational companies (MNCs)1 are of tremendous importance for the world economy. They account for more than one-third of global production, around half of worldwide exports, and about a quarter of global employment (Cadestin et al. (2018), p. 4; Cadestin et al. (2019), p. 8). Of particular importance for MNCs are foreign subsidiaries (Kim et al. (2005), p. 44; Kretschmer (2008), p. 1; Dörrenbächer/Gammelgaard (2016), p. 1250). In fact, foreign subsidiaries import and export more goods and services than MNCs’ head offices and domestic subsidiaries (Kim et al. (2005), p. 44; Dörrenbächer/Gammelgaard (2016), p. 1250; Cadestin et al. (2019), p. 10). Furthermore, the sales of foreign subsidiaries have increased by more than 380% in value between 1990 and 2018 according to latest figures of the World Investment Report (UNCTAD (2019), p. 18).

Due to this high importance of foreign subsidiaries for MNCs, it is undoubted that head offices need effective mechanisms to control their subsidiaries (Roth/Nigh (1992), pp. 277-279; Egelhoff (2010), pp. 420-428).2 The management accounting literature suggests that performance measurement systems (PMSs), which head offices implement at their subsidiaries (parent-PMSs), can fulfill this role:

“Parent-PMS portray an important control mechanism in MNCs as they reflect the intentions of headquarters and are able to improve relationships between headquarters and subsidiaries. They translate subsidiary activities into measurable outcomes and provide a common basis for decision-making at all levels of the MNC, including foreign subsidiaries.”

(Mahlendorf et al. (2012), p. 689)3

As pointed out in the literature, head offices pursue two objectives with parent-PMSs (Dossi/Patelli (2008), pp. 128-131; Mahlendorf et al. (2012), p. 689; Wu (2015), pp. 9-11).4 First, head offices employ parent-PMSs to obtain performance information on their worldwide-dispersed subsidiaries to facilitate decision-making (Austin (1996), pp. 25-28; Quattrone/Hopper (2005), p. 742; Horváth/Seiter (2009), p. 396). Information on the performance of the subsidiaries allow head offices, for example, to allocate resources within the MNC (Kaplan/Norton (2001), p. 158; Henri (2006), p. 77; Dossi/Patelli (2008), p. 132). Second, head offices implement parent-PMSs to influence the decisions of the subsidiaries (Dossi/Patelli (2008), p. 131). This is to ensure that the subsidiaries contribute to the overall goals of the MNCs rather than pursuing local goals (Mahlendorf et al. (2012), p. 689; Wu/Schäffer (2015), p. 109). Given these two important objectives of parent-PMSs, it is not surprising that these systems are widespread in practice. For example, Dossi/Patelli ←1 | 2→show that almost all head offices in their sample implement parent-PMSs at their subsidiaries (Dossi/Patelli (2008), p. 134).

However, despite the high importance practitioners and scholars attach to parent-PMSs, two research gaps on parent-PMSs are prevailing in the management accounting literature. First, research has neglected important developments concerning the design of parent-PMSs. Admittedly, research on the design of parent-PMSs has a long-lasting tradition, but older empirical studies (e.g. McInnes (1971); Choi/Czechowicz (1983)) mainly deal with financial performance measures and targets only (Schmid/Kretschmer (2010), p. 225). However, nowadays parent-PMSs are no longer regarded as purely financial systems (Chenhall/Langfield-Smith (2007), p. 267). Instead, the literature suggests that the design of parent-PMSs has changed during the last decades in several ways (Bourne et al. (2000), pp. 754-755; Klingebiel (2001), pp. 17-18; Gleich (2011), pp. 10-19). First, parent-PMSs today are expected to contain both financial and non-financial performance measures and targets (Lynch/Cross (1995), p. 38; Klingebiel (2001), pp. 17-18). Second, conceptual studies suggest that parent-PMSs should be linked to the remuneration of the subsidiaries’ management and staff to effectively influence their decisions (Atkinson (1998), pp. 553-556; Otley (1999), p. 366). Finally, it is common sense that parent-PMSs nowadays need an information technology (IT) infrastructure, which consists of, for example, enterprise resource planning systems and business intelligence systems (Horváth/Seiter (2009), p. 402; Heinicke (2018), p. 480).

Despite this newer and broader understanding of parent-PMSs, many studies (e.g., Quattrone/Hopper (2005); Kihn (2008)) still only address single design elements of parent-PMSs, such as performance measures or IT systems. By providing descriptions of single elements, these studies cannot describe how the different design elements of parent-PMSs are connected to each other. Furthermore, many studies (e.g., Kihn (2008); Dossi/Patelli (2010); Du et al. (2013) have an explanatory focus and therefore do not describe the design of parent-PMSs in detail. Thus, the management accounting literature lacks a description of the design of parent-PMSs based on multiple design elements.

The second research gap relates to the adoption of parent-PMSs at subsidiary level, which has received scant attention in the literature:

“For multinational enterprises (MNEs), the adoption of practices by various subsidiaries remains an interesting but insufficiently discussed management issue […]. This issue requires attention from both researchers and managers because it affects the managerial performance of MNEs.”

(Cheng/Yu (2012), p. 82)

“There are not many studies in the accounting literature which explore whether and how locals reshape global management control systems when mobilising them to conduct their day-to-day activities. […] It seems to be assumed, therefore, that the management control systems used by the parents will simply be reproduced […].”

(Cruz et al. (2011), p. 414)

←2 | 3→As expressed by the quotes above, the literature has ignored how subsidiaries adopt parent-PMSs for a long time (Dossi/Patelli (2008), p. 144; Cruz et al. (2011), p. 414). In fact, the literature has mainly looked at the design of these systems or has simply assumed that subsidiaries adopt parent-PMSs as intended by the head offices (Cruz et al. (2011), p. 414). However, recent studies (e.g., Siti-Nabiha/Scapens (2005); Dossi/Patelli (2008); Mahlendorf et al. (2012)) provide preliminary evidence that subsidiaries might deviate from head offices’ intentions in two ways when adopting parent-PMSs.

First, the subsidiaries’ use of the parent-PMS might deviate from head offices’ intentions (Dossi/Patelli (2008), p. 138; Mahlendorf et al. (2012), p. 689). In fact, the few existing studies indicate that subsidiaries might only pretend to use parent-PMSs without actually incorporating them in the day-to-day business (Siti-Nabiha/Scapens (2005), p. 58; Dossi/Patelli (2008), p. 138; Mahlendorf et al. (2012), p. 689). For example, subsidiaries might report the performance measures of the parent-PMS to their head office but do not discuss them in local meetings (Ansari/Euske (1987), pp. 561-564; Siti-Nabiha/Scapens (2005), p. 47). Second, the management accounting literature provides evidence that subsidiaries might develop their own PMS when they are dissatisfied with the design of the parent-PMS (e.g., Siti-Nabiha/Scapens (2005), p. 65; Dossi/Patelli (2008), p. 140). These so-called local-PMSs are unofficial PMSs, which are not approved by the MNCs’ head offices (Kilfoyle et al. (2013), pp. 385-386; Goretzki et al. (2018), pp. 1888-1892). A subsidiary might develop a local-PMS to have an alternative to the parent-PMS or to compensate for the perceived weaknesses in the parent-PMS design (Siti-Nabiha/Scapens (2005), p. 65; Cruz et al. (2011), p. 413; Cooper/Ezzamel (2013), pp. 291-293).

When subsidiaries adopt parent-PMSs differently than expected by their head offices, the parent-PMSs might not have the head offices’ desired effects (Siti-Nabiha/Scapens (2005), p. 58; Dossi/Patelli (2008), p. 140; Rehring (2012), p. 96). Since this jeopardizes the overall goals of the MNCs (Mahlendorf et al. (2012), p. 705; Wu (2015), p. 10), the adoption of parent-PMSs should be considered in more detail. In particular, several aspects deserve further attention. First, quantitative studies on the use of parent-PMSs only examine the extent to which subsidiaries use the parent-PMSs but do not describe how subsidiaries use these systems. The existing qualitative studies mainly examine the use of parent-PMSs at domestic subsidiaries or joint ventures. Thus, the literature lacks a detailed description of different usage types of parent-PMSs. Second, most prior studies (e.g., Dossi/Patelli (2008); Schäffer et al. (2010) only document the existence of local-PMSs but not describe the design of these unofficial PMSs.5 This hinders understanding how the local-PMSs differ from the parent-PMSs implemented by the head offices. Moreover, most prior studies (e.g., Dossi/Patelli (2008); Schäffer et al. (2010)) examine the use of parent-PMSs and the development of local-PMSs separately. Therefore, there is no study providing a typology of the adoption of parent-PMSs. Finally, little is known about the factors that influence how subsidiaries adopt parent-PMSs. Prior studies only indicate that subsidiaries deviate from head offices’ intentions in adopting parent-PMSs because standardized parent-PMSs “do not fully interpret the local contexts or satisfy local demands” (Wu/Schäffer (2015), p. 109; cf. also Vance (←3 | 4→2006), p. 42). However, scant evidence exists on the parent-PMS characteristics (e.g., subsidiaries’ participation in the parent-PMS design) that affect the adoption of parent-PMSs. Furthermore, little is known about the local contexts (e.g., national culture) that influence how subsidiaries adopt parent-PMSs. Hence, management accounting research should examine how parent-PMSs are adopted at subsidiary level and what influences this adoption.

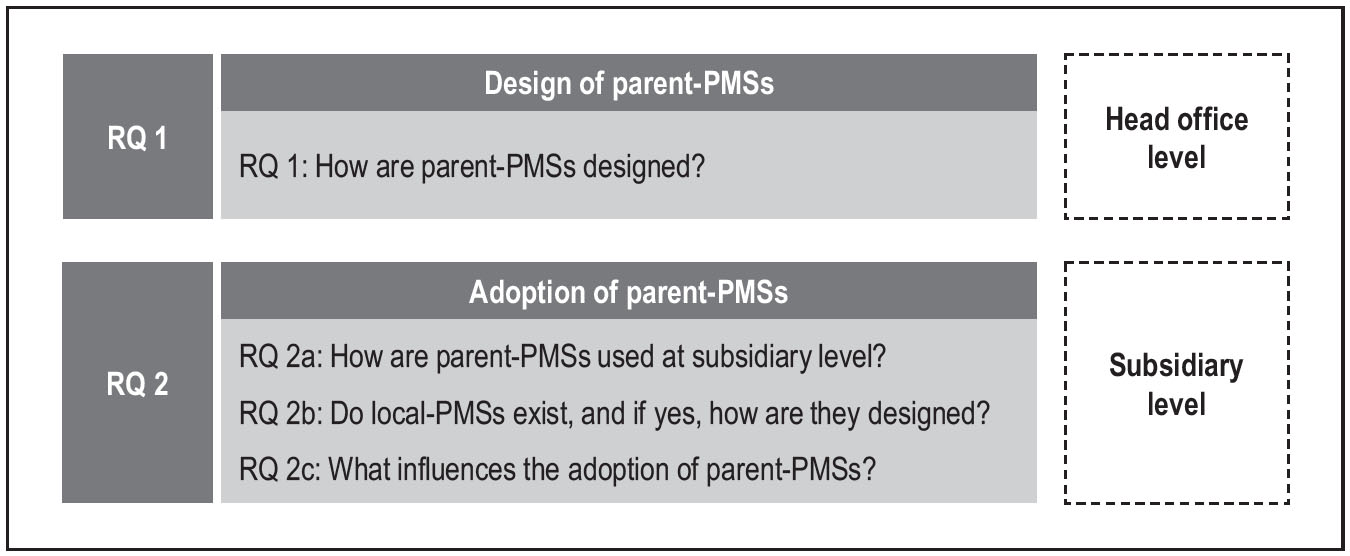

Overall, research is needed on the design and adoption of parent-PMSs in MNCs. Consequently, this study addresses both topics by answering the research questions depicted in Figure 1–1.

The first research question (RQ) relates to the head office level. It aims to provide a description of the design of the head offices’ parent-PMSs. This description also serves as the basis for investigating the second research questions, which shift the focus to the adoption of parent-PMSs at subsidiary level. RQ 2a seeks to describe how the subsidiaries use the parent-PMSs. By addressing RQ 2b, this study aims at investigating the existence and design of local-PMSs. Based on the use of parent-PMSs and the existence and design of local-PMSs, this study intends to carve out a typology of the adoption of parent-PMSs. Finally, RQ 2c aims at exploring factors that influence how the subsidiaries adopt parent-PMSs.

These research questions are addressed by conducting case studies of five German MNCs. This research approach is particularly suitable due to the explorative stage of prior research, especially on the adoption of parent-PMSs. At each case company, interviews are conducted at both head office and subsidiary level. The interviews at head office level provide information on the design of the parent-PMSs. At subsidiary level, experts from two subsidiaries of each case company are interviewed to examine the adoption of the parent-PMSs. The resulting empirical data is analyzed both within and across the cases.

Addressing these research questions contributes to management accounting research and practice in several ways. First, this study describes the design of parent-PMSs based on multiple elements, which allows the designers of parent-PMSs in MNCs’ head offices to compare the design of their own parent-PMS with the design of other parent-PMSs. Second, examining how subsidiaries use parent-PMSs enhances researchers’ understanding of the differences between a functional and dysfunctional use. This is also relevant for designers ←4 | 5→of parent-PMSs, as it shows how subsidiaries can deviate from head offices’ intentions when using parent-PMSs. Third, this study contributes to management accounting research and practice by carving out characteristics of local-PMSs and by describing the design of these systems. This sharpens the distinction between parent-PMSs and local-PMSs. Furthermore, the typology of the adoption can be used by other researchers when examining, for example, the prevalence of the different adoption types. Finally, identifying factors that influence the adoption supports management accountants in MNCs’ head offices in developing parent-PMSs that are adopted by the subsidiaries in accordance with their intentions.

Details

- Pages

- XXIV, 284

- Publication Year

- 2020

- ISBN (Hardcover)

- 9783631821930

- ISBN (PDF)

- 9783631828557

- ISBN (ePUB)

- 9783631828564

- ISBN (MOBI)

- 9783631828571

- DOI

- 10.3726/b17231

- Language

- English

- Publication date

- 2020 (May)

- Keywords

- multinational corporations design choices performance measures adoption types decoupling case study institutional theory expert interviews Performance Measurement

- Published

- Berlin, Bern, Bruxelles, New York, Oxford, Warszawa, Wien, 2020. XXIV, 284 pp., 90 fig. b/w, 41 tables

- Product Safety

- Peter Lang Group AG